,

,Received(Settlement: DateTime; Maturity: DateTime; Investment: Double; Discount: Double; [Basis: Integer = 0]): Double;

Settlement. The payment day on securities. Must be less than Maturity

Maturity. The security's maturity date. Must be greater than Settlement

Investment. The amount invested in securities. Must be positive

Discount. Discount for a security. Must be in the [0, B/DIM] range, where B - the number of days in a year and DIM - the number of days from issue date to maturity date.

Basis. The day calculation method used. Select a value from 0 to 4:

0. Day calculation method - American/360 days (NSAD method). Default value.

1. Day calculation method - Actual/actual.

2. Day calculation method - Actual/360 days.

3. Day calculation method - Actual/365 days.

4. Day calculation method - European 30/360 days.

Optional parameter.

The Received method returns the sum, received by the maturity date of the fully secured securities.

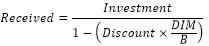

Recieved is calculated using the following formula:

,

where:

B. The number of days in a year (depends on the selected Basis argument value).

DIM. The number of days from issue date to maturity date.

Add a link to the MathFin system assembly.

Sub UserProc;

Var

r: Double;

Begin

r := Finance.Received(DateTime.ComposeDay(2008,01,01), DateTime.ComposeDay(2008,06,01), 1500.5, 0.15, 0);

Debug.WriteLine(r);

End Sub UserProc;

After executing the example the console window displays the sum equal to 1600.53.

See also: