.

.MDuration(Settlement: DateTime; Maturity: DateTime; CouponRate: Double; YieldP: Double; Frequency: Integer; [Basis: Integer = 0]): Double;

Settlement. The payment day on securities. Must be less than Maturity.

Maturity. The security's maturity date. Must be greater than Settlement.

CouponRate. Annual interest rate for coupons on securities. Must be positive.

YieldP. The annual income on securities. Must be positive.

Frequency. The annual number of coupon payments. The parameter can take the following values:

1. Annual payments.

2. Semi-annual payments.

4. Quarterly payments.

Basis. The day calculation method used. Select a value from 0 to 4:

0. Day calculation method - American/360 days (NSAD method). Default value.

1. Day calculation method - Actual/actual.

2. Day calculation method - Actual/360 days.

3. Day calculation method - Actual/365 days.

4. Day calculation method - European 30/360 days.

Optional parameter.

The Mduration method returns a modified Macaulay duration for securities with supposed face value of $100.

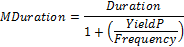

Mduration is calculated using the following formula:

.

To get Macaulay duration, use the IFinance.Duration method.

To execute the example, add a link to the MathFin system assembly.

Sub UserProc;

Var

r: Double;

Begin

r := Finance.Mduration(DateTime.ComposeDay(2008,01,01), DateTime.ComposeDay(2016,01,01), 0.28, 0.82, 4, 3);

Debug.WriteLine(r);

End Sub UserProc;

After executing the example the console window displays modified Macaulay duration equal to 1.243.

See also: