In statistics the Generalized Pareto Distribution (GPD) is a set of continuous probability distributions. It is often used for modeling of other distributions tails.

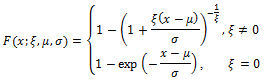

Assume that the random variable X is distributed by the rule, described by the function:

For x ≥ μ when ξ ≥ 0 and μ ≤ x ≤ μ - σ / ξ when ξ < 0, where:

![]() . Layout parameter.

. Layout parameter.

σ > 0. Scale parameter.

![]() . Form parameter.

. Form parameter.

Then random value X has the Generalized Pareto Distribution or ![]() .

.

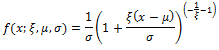

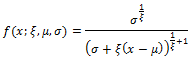

Distribution density function:

Or

If μ ≤ x ≤ μ - σ / ξ when ξ < 0.

Mean:

![]()

Variance:

![]()

Median:

![]()

Generalized Pareto distribution does not have skewness and kurtosis coefficients.

Log-likelihood function for GPD:

![]()

For x ≥ μ when ξ ≥ 0 and μ ≤ x ≤ μ - σ / ξ when ξ < 0.

To find optimal parameters estimation, maximize ln L(ξ, μ, σ).

See also:

Library of Methods and Models | ISmGeneralizedParetoDistribution