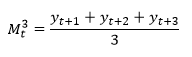

Centered moving average method

Centered moving average methodThe moving average method is based on representing a series as a sum of sufficiently smooth trend and a random component. Moving averages need to be estimated when it is not clear, which function must be selected for a trend.

Available calculation methods:

Centered moving average method

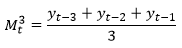

Backward moving average method

See also:

Modeling and Forecasting: Model | IModelling.Movavg | ISmSlideSmoothing